Over the past few years, you have consistently heard about Blockchain technology, especially concerning Bitcoin, cryptocurrencies, or NFT. It’s majorly because of its wide application across various industries. Blockchain has proved to be a remarkable invention of the 21st Century, given the ripple effect on numerous sectors. Start from finance to manufacturing, real estate, healthcare, and more. Blockchain’s value lies in its ability to quickly and securely share data among stakeholders, while reducing transaction facilitation and safeguarding responsibilities.

Blockchain software development companies are assisting enterprises globally in implementing this technology trend to business systems and streamlining their overall operations. Blockchain-based applications are becoming a robust alternative to traditional business models making businesses faster, more efficient, and cost-effective.

Why Businesses Prefer Blockchain Over Traditional Databases

A significant difference between traditional databases and blockchain is the architecture of the database. A standard database stores data in tables and follows a centralized architecture to collect crucial data in a fixed format or fields. On the other hand, a blockchain collects information in groups, known as blocks. Once the block threshold for storing transactions is attained, the blockchain links it to the previously filled block by utilizing the SHA-256 hashing mechanism, which enhances security and guarantees that the data is stored in a decentralized and distributed manner. Furthermore, by using this method, the blockchain can enable more efficient and transparent transactions compared to traditional databases.

Blockchain guarantees the security and fidelity of the recorded transactions with timestamps stored in the digital ledger and maintains trust between stakeholders without needing a trusted third party. On the other hand, traditional databases lack security due to insufficient IT security expertise and require an administrator to function.

Each blockchain participant has a safe copy of all records and modifications, allowing each user to see data provenance, a feature that traditional databases do not offer.

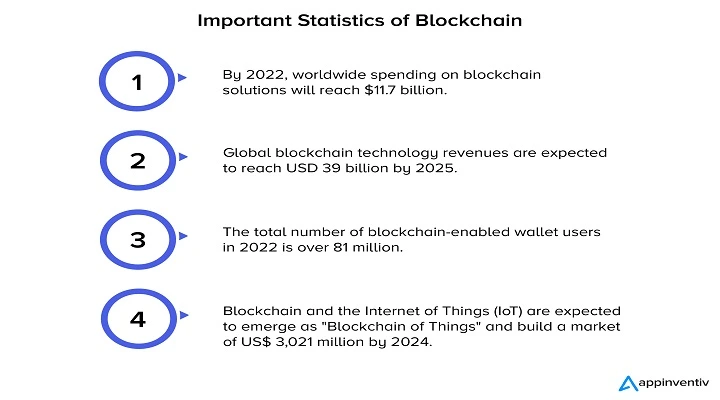

Important Statistics of Blockchain

Blockchain applications across various industries have increased in the last few years. Large enterprises invest vast chunks of money in blockchain to streamline their business supply chains at all levels. Here are some vital statistics about blockchain you must know:

- By 2022, worldwide spending on blockchain solutions will reach $11.7 billion.

- Statista states global blockchain technology revenues are expected to reach USD 39 billion by 2025.

- The total number of blockchain-enabled wallet users in 2022 is over 81 million.

- Blockchain and the Internet of Things (IoT) are expected to emerge as “Blockchain of Things” and build a market of US$ 3,021 million by 2024.

Now that you’re familiar with blockchain statistics and have an idea about its growth projections for the future, it’s time to know the significant aspects of blockchain.

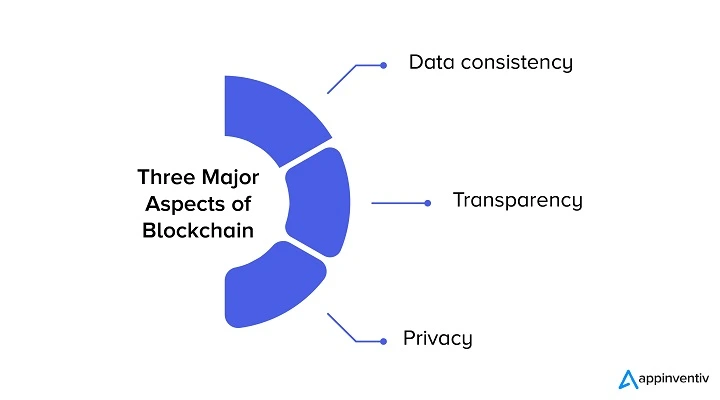

The Three Major Aspects of Blockchain

Data Consistency

Data consistency is defined when all participants receive the same data throughout the network. The blockchain network is decentralized means there’s no central governing authority. A group of nodes maintain the network and conducts and approve activities on the blockchain platform, also known as the process of reaching consensus.

Blockchain technology uses data blocks and transaction mechanisms where participants can host different information patterns. These nodes constantly verify data integrity and validity via consensus algorithms and agree upon transaction execution. Any validated records are irreversible and can’t be altered, meaning no network user can edit, change, or delete them.

Blockchain technology empowers participants to summaries informational datasets and hash the information to keep a record. You can track the data consistency for each node by using the transaction hash ID. One major issue of using blockchain for data consistency is hashing individual rows can be really expensive as it’ll consume ample storage space on the network.

However, such costs can be mitigated using reduced versions of the hashes. For instance, rather than storing the numerical value of individual transactions, you can store the hashed summary of your transactions.

Transparency

Data transparency makes blockchain unique, making many users argue for using blockchain as the new standard for transparency. Blockchain works on the distributed ledger technology means that all network participants have a copy of the ledger for complete transparency.

A public ledger contains comprehensive information about the blockchain network’s participants and transactions. Tracking a distributed ledger is easy since changes propagate quickly throughout the network. Any updates to the ledger are reflected within seconds or minutes. Additionally, adding a block follows a standard procedure without any nodes receiving special treatment or favors from the network.

Also, blockchain technology provides encryption and validation methods to safeguard user data. In the blockchain, network participants can access holdings and transactions of public addresses using block explorers and public keys. However, data can only be manipulated, modified, or deleted only once the network consensus has validated it. If anyone tries to change the transaction, every other network block would have to be altered, which is next to impossible.

Privacy

Blockchain allows users to keep control of their data while providing a secure data storage option. A key aspect of blockchain privacy is using private and public keys. The blockchain systems are built using asymmetric cryptography to secure transactions between users in a public ledger.

It is impossible for users to guess other private keys as its mathematically impossible. For exchanging limited data, users can share their public keys as they do not reveal personal information, which increases security.

Each user has an address derived from the public key using hash functions.

The network stakeholders’ servers employ a rapid consensus algorithm to authenticate transactions that utilize these addresses while concealing user identities.

Conclusion

One considers Blockchain as one of the most disruptive technologies across all industries. This technology is vastly essential in the financial services industry and the field of supply chain and logistics. Many software development companies are assisting enterprises of all sizes in solving the data storing issues they have gleaned over the years.

In the future blockchain will experience more advancements with pragmatic governance models, better interconnectivity, and adjacent technologies combined to provide faster, reliable, and accurate results for successful business automation and growth.